2017 AP Microeconomics FRQ #3

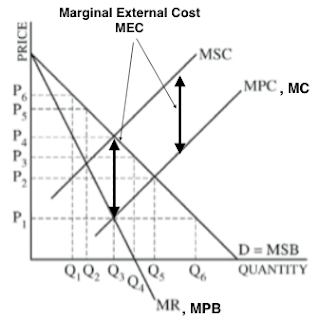

(A) Identify the monopolists.

(i) Profit maximising quantity

(ii) Profit maximising price

Recognise, that the MPC is the MC curve and that the MR = MPB, therefore the Profit Max for this Monopoly is where MR = MC,

Price = P4

Quantity = Q3

Answer

(B) What information in the graph indicates that there is a negative externality?

MSC > MPC = Negative Externality

Answer

(C) Identify the socially optimal quantity.

Social Optimal Quantity is where MSB = MSC

Social Optimal Quantity = Q3

|

| Understand: This time the monopoly is producing an output that is equal to the socially efficient amount, Here the welfare losses caused by the negative externality are less in a monopoly environment than they would be in a competitive environment. This is a point worth remembering when it comes to things like energy markets. People naturally assume that competitive markets are better than ones with market power, but if there is a negative externality of pollution that comes with consuming energy, then the economic welfare effects may be less bad for society if there is a monopoly or oligopoly provider producing a lower amount at higher price for consumers (and enjoying high profits) than if there was a competitive market, prices were forced down for consumers, and an excessive amount of energy was consumed. |

Answer

(D) In the case in which the government imposes a per-unit tax equal to the marginal external cost, identify each of the following.

(i) The dollar value of the tax, using the price labels from the graph

The tax would be equal to the vertical distance between the MSC and MPC. (P4 - P1)

The tax would be equal to the vertical distance between the MSC and MPC. (P4 - P1)

(ii) The profit-maximising quantity associated with the tax.

Answer

(E) Given the monopoly facing the negative externality, would the dead-weight loss increase, decrease, or stay the same as a result of imposing the per-unit tax? Explain.